Bankruptcy is often misunderstood and could actually lead to a life of financial peace.

[/vc_column_text][divider line_type=”No Line” custom_height=”8″][divider line_type=”No Line” custom_height=”8″][divider line_type=”No Line” custom_height=”8″][divider line_type=”No Line” custom_height=”8″][divider line_type=”No Line” custom_height=”8″][/vc_column][/vc_row][vc_row type=”in_container” full_screen_row_position=”middle” scene_position=”center” text_color=”dark” text_align=”left” overlay_strength=”0.3″ shape_divider_position=”bottom”][vc_column column_padding=”no-extra-padding” column_padding_position=”all” background_color_opacity=”1″ background_hover_color_opacity=”1″ column_shadow=”none” column_border_radius=”none” width=”1/1″ tablet_text_alignment=”default” phone_text_alignment=”default” column_border_width=”none” column_border_style=”solid”][vc_column_text]Even with the most meticulous planning and as much as we try to avoid it, financial hardship and bankruptcy can happen to anyone. Also, with many myths surrounding it, bankruptcy is often dismissed as a viable solution for many Auburn or Opelika residents. Some even believe that filing for bankruptcy means the end of their finances forever. However, bankruptcy is often misunderstood and could actually lead to a life of financial peace.Despite that, deciding whether or not to file for bankruptcy is a major decision that requires careful consideration. So, here are three signs that may indicate it’s time to speak with a bankruptcy attorney about your options from David S. Clark, an experienced personal bankruptcy attorney in Opelika, Alabama. [/vc_column_text][/vc_column][/vc_row][vc_row type=”in_container” full_screen_row_position=”middle” scene_position=”center” text_color=”dark” text_align=”left” overlay_strength=”0.3″ shape_divider_position=”bottom”][vc_column column_padding=”no-extra-padding” column_padding_position=”all” background_color_opacity=”1″ background_hover_color_opacity=”1″ column_shadow=”none” column_border_radius=”none” width=”1/3″ tablet_text_alignment=”default” phone_text_alignment=”default” column_border_width=”none” column_border_style=”solid”][vc_column_text css=”.vc_custom_1582649947294{background-color: #dddddd !important;}”]

DISCLAIMER: The following blog post is just advice, and you will be better served to call David S. Clark with your bankruptcy questions. This blog contains helpful tips and advice, but is not professional legal advice, and shouldn’t treated as such.

[/vc_column_text][divider line_type=”No Line” custom_height=”8″][nectar_cta btn_style=”see-through” heading_tag=”h6″ text_color=”#6d1839″ link_type=”regular” alignment=”left” text=”Need Bankruptcy Help?” link_text=”Call David S. Clark” url=”tel:3347493800″][social_buttons facebook=”true” twitter=”true” google_plus=”true”][/vc_column][vc_column column_padding=”no-extra-padding” column_padding_position=”all” background_color_opacity=”1″ background_hover_color_opacity=”1″ column_shadow=”none” column_border_radius=”none” width=”2/3″ tablet_text_alignment=”default” phone_text_alignment=”default” column_border_width=”none” column_border_style=”solid”][vc_column_text]Overwhelming Debt

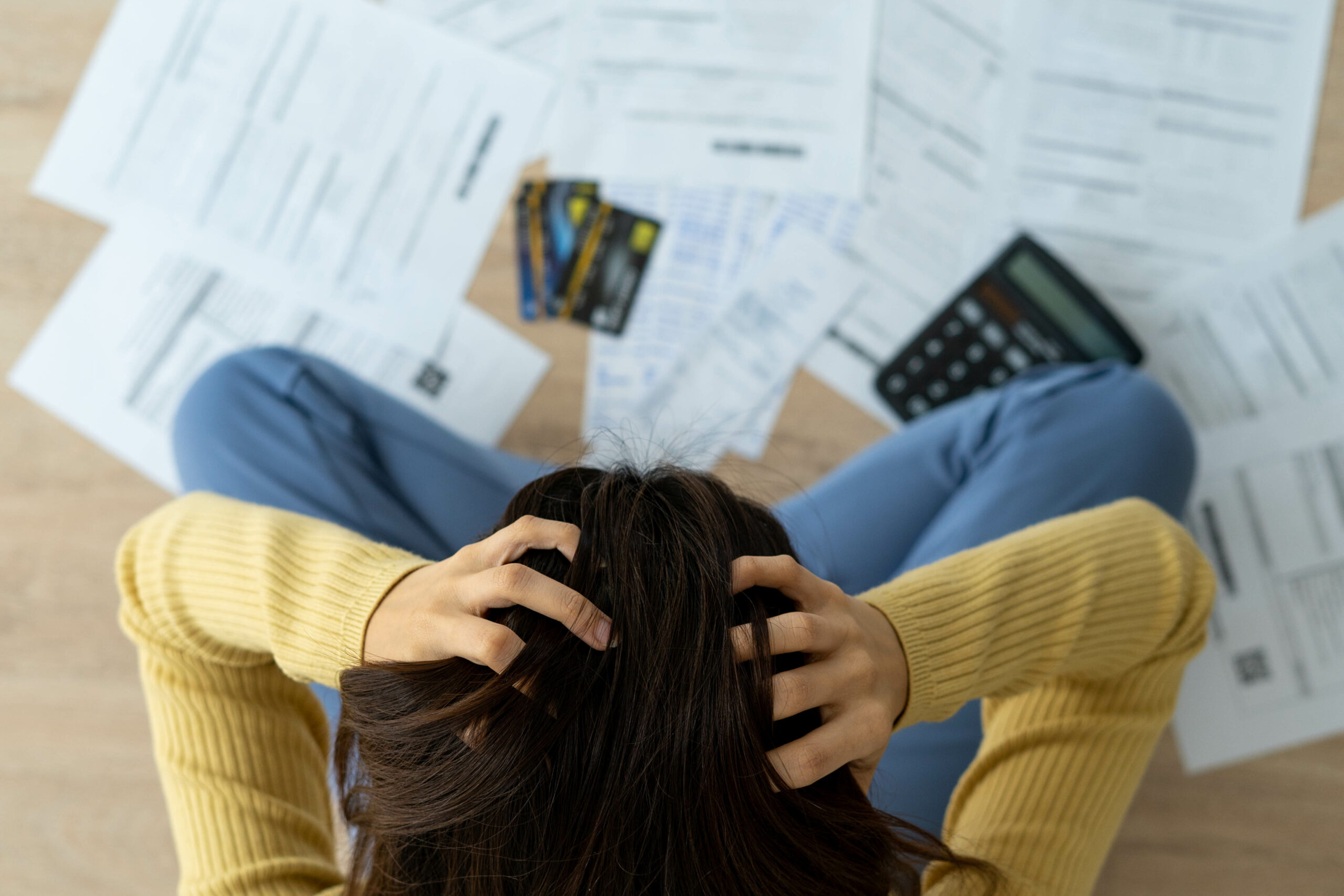

When the weight of debt becomes seemingly unmanageable, it can be challenging to pay even the minimum amount owed. This not only leads to deeper debt but can even add a significant burden to your daily life. More debt can also lead to late fees, penalties, and interest charges, making it even harder to get out of debt.

Unmanageable debt is often a strong indication that it may be time to talk to an experienced bankruptcy attorney about your options. Depending on your situation, Chapter 7 or Chapter 13 bankruptcy may be able to help by consolidating your debts and allowing you to make more manageable payments. In some cases, it may even be possible to discharge some or all of your debts, giving your finances a fresh start.

Debt Collection Harassment & Threats of Legal Action

Beyond the effect that overwhelming debt can have on you and your family, creditors can sue you for non-payment of debt, leading to wage garnishment, property liens, or even the seizure of a number of your assets.

Thankfully, filing for Chapter 7 or Chapter 13 bankruptcy can halt legal action and protect your valuable assets. When you file for bankruptcy, an automatic stay goes into effect, which puts an immediate stop to creditor actions, including lawsuits and wage garnishment.

Lack of Savings

While the lack of a savings account does not mean bankruptcy, it can act as a warning of what could happen in the future. Ultimately, without a financial cushion, a single unexpected expense, such as a medical emergency, car repair, or job loss, can quickly spiral into financial distress.

Filing for bankruptcy can help you get back on your feet by giving you a fresh start. It can discharge your debts, freeing up your income to rebuild your savings and secure your financial future[/vc_column_text][/vc_column][/vc_row][vc_row type=”in_container” full_screen_row_position=”middle” scene_position=”center” text_color=”dark” text_align=”left” overlay_strength=”0.3″ shape_divider_position=”bottom”][vc_column column_padding=”no-extra-padding” column_padding_position=”all” background_color_opacity=”1″ background_hover_color_opacity=”1″ column_shadow=”none” column_border_radius=”none” width=”1/1″ tablet_text_alignment=”default” phone_text_alignment=”default” column_border_width=”none” column_border_style=”solid”][vc_column_text]

David S. Clark, Your Auburn & Opelika Personal Bankruptcy Attorney

In conclusion, if you are struggling with overwhelming debt or facing legal action from creditors in Alabama, filing for bankruptcy may be a viable solution. However, it’s essential to speak with an experienced bankruptcy attorney in Alabama to understand your options.

At David S. Clark, we are dedicated to helping our clients in Auburn or Opelika achieve financial freedom. Contact us today to schedule a free consultation and learn more about how we can help you with Chapter 7 or Chapter 13 bankruptcy. [/vc_column_text][/vc_column][/vc_row][vc_row type=”in_container” full_screen_row_position=”middle” bg_color=”#dddddd” scene_position=”center” text_color=”dark” text_align=”left” overlay_strength=”0.3″ shape_divider_position=”bottom” shape_type=””][vc_column column_padding=”padding-7-percent” column_padding_position=”all” background_color_opacity=”1″ background_hover_color_opacity=”1″ column_shadow=”none” column_border_radius=”none” width=”1/1″ tablet_text_alignment=”default” phone_text_alignment=”default” column_border_width=”none” column_border_style=”solid”][vc_column_text]

DISCLAIMER: The above blog post is just advice, and you will be better served to call David S. Clark with your bankruptcy questions. This blog contains helpful tips and advice, but is not professional legal advice, and shouldn’t treated as such.

[/vc_column_text][/vc_column][/vc_row]